Charting the UK's Supplement eCommerce Surge

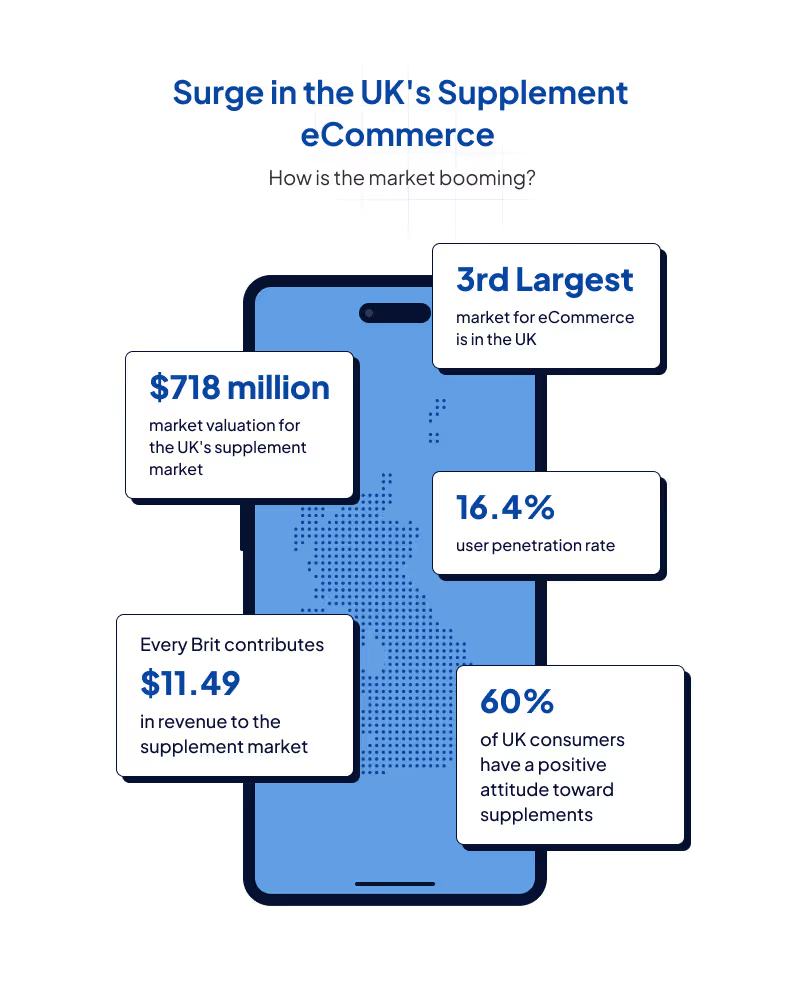

The United Kingdom’s dietary supplement market, valued at $718 million, might seem like a gentle giant compared to the US’s $4.58 billion and China’s $5.33 billion behemoths. However, despite the seemingly modest number, there's more to the UK's supplement market than meets the eye.

By 2029, there will be 11.9 million supplement users in the UK, as the user penetration is expected to grow from 16.4% in 2024 to 18.4% in 2029. This booming demand is a strong indicator of the UK’s ballooning appetite for dietary supplements, and we’re keeping a close watch to see how it’s evolving.

The 30,000-foot view of the supplement market

Between 2018 and 2023, the UK’s supplement market has grown 25% in value, and it’s forecasted to grow 10% each year from 2023 to 2028. Let’s take a bird’s eye view of the UK’s market to understand its composition better.

- The UK has the third-largest market for eCommerce in the world.

- Italy, Germany, France, and the UK comprise 70% of the European supplement market. However, UK consumers have the most positive attitude towards supplements.

- Presently, the UK’s supplement market has a 40.1% online share. That means 4 out of 10 consumers buy their supplements online! This share is expected to rise to 44.9% by 2028.

- Market share for online-only supplement retailers in the UK is rather low. As a result, the top four brands in the segment contribute less than 40% to the total industry revenue.

- Vitamin D leads the market race at 42%. Vitamin C (31%), general multivitamins (33%), and Omega 3 (25%) follow close behind in user preference.

- The UK’s ARPU (Average Revenue Per Unit) will reach $2673.71 by 2029, translating to higher consumer spending on average. For comparison, the US’s ARPU is roughly $3000 in 2024.

- Given the UK’s total population, every Brit contributes $11.49 (approx.) in revenue to the supplement market.

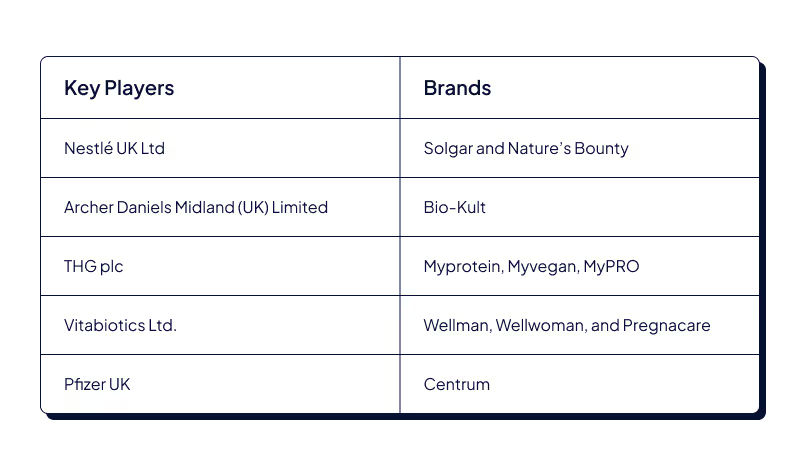

- Here are five of the leading players in the UK’s supplement market.

What’s painting the market green? Rising demand fuels consumer spending

The global demand for supplements is stronger than ever, with the industry (valued at $177.5 billion in 2023) projected to grow by 9.1% each year from 2024 to 2030. This positive sentiment is already trickling down to the UK’s expanding market, as the number of supplement users is growing yearly.

More and more consumers are also loosening purse strings and spending freely. This comes as a relief after the inflationary burns of 2022 and 2023.

Today, Brits are less price-conscious about spending (down to 52.4% from 61.5% in 2023), but especially the younger generation, who are throwing caution to the wind compared to the older lot and spending more.

- Consumers aged 18-24: spending freely

- Consumers aged 55-64: spending most cautiously

And it’s not just the aging generation pooling money into supplements. While the geriatric population remains the highest consumer of supplements, Gen Z and millennial Brits are buying more supplements than the booming generation. They are relying on dietary supplements for two main reasons:

- They want to supplement the nutrients they get from the diet (55%)

- They want to boost their immune system (53%)

Besides, platforms like Instagram and TikTok are also vital in fueling the demand for supplements, with many wellness influencers turning Brits towards preventative care and influencing their spending preferences.

Interestingly, after seeing how much consumers searched for supplements and interacted with related brands (from 22.1% in 2023 to 33.1% in 2024), TikTok even went a step ahead and set up a shop right in its app.

The social media giant teamed up with major supplement and wellness brands for TikTok Shop UK last year, allowing audiences to discover and buy a product within the app. This, among other platform features, has positively impacted supplement sales.

For example, Healthxcel, a certified wellness brand selling natural and organic superfood powders, saw a 400% rise in sales after launching a TikTok campaign using its ad platform, Spark Ads.

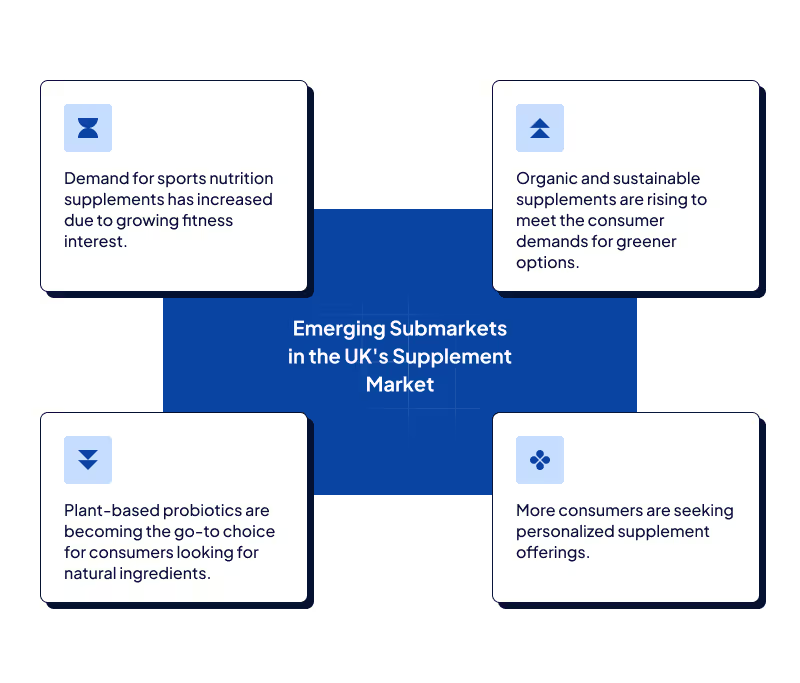

However, the UK’s supplement market isn’t a monolith. It accommodates and caters to a variety of consumer preferences and nutritional needs. Presently, there are four submarkets with the most potential.

Let’s explore them in detail.

The map isn’t the territory: Where the real opportunities lie

We noticed four emerging submarkets in the UK’s supplements market.

These cater to evolving consumer demands and offer lucrative opportunities for brands looking to expand portfolios or enter the supplement category.

- Sports Nutrition is the talk of the town. As interest in fitness and body-building burgeons, many gym-goers and fitness enthusiasts are turning to sports nutrition supplements like probiotic tablets, whey protein, collagen repair, and more. However, not many are fully satisfied with the available products. 50% of consumers want a wider range of natural sports nutrition alternatives, suggesting a strong market for products made with natural ingredients.

- Consumers are more environmentally conscious and ready to pay a premium for greener options. Until 2023, most consumers (53.6%) didn’t want to pay anything extra for a green product. However, there was a behavioral shift moving into 2024. That figure has since declined to 41.4% as consumers, specifically those under 35, are okay with shelling out more for a green product. This opens doors for brands offering organic and sustainable supplement options.

- Demand for plant-based probiotics is booming, with consumers increasingly seeking organic, natural, and vegan supplement options. The UK's probiotics market size is estimated at $1.91 billion in 2024, a good 3% of the global industry valued at $71.2 billion. However, what's interesting is that the European probiotics market, estimated at $13.78 billion, holds the second biggest market share after Asia-Pacific and offers significant room for probiotic expansion.

- More consumers are seeking personalized supplement offerings. According to a survey by The Grocer, UK’s FMCG-focused magazine, consumers are ready to pay more for products tailored to specific needs such as health conditions or life stage (40%), easier-to-understand descriptions (36%), more advice from staff (27%), and easier-to-navigate fixtures (13%).

The undervalued gem: How D2C can shine as a distribution channel

Despite having the 6th largest economy globally, a strong eCommerce foothold, and a growing number of supplement users, the UK market has yet to peak. Higher shipping costs, poor delivery experiences, and a lack of personalized services often hinder sales growth.

By offering direct customer interactions, higher brand equity, and faster product development and testing, DTC, as a channel, can fill this gap.

Data shows that 48% of Brits prefer shopping outside their domestic market. They buy cross-border from China (57%), followed by the US (47%) and Germany (11%) by placing orders directly on the brand’s website. When asked why, the shoppers surveyed provided two reasons for doing so:

- Affordability concerns: Shopping from international brands with low shipping costs is allegedly cheaper than shopping locally.

- A wider variety of products: They’re drawn to diverse and unique offerings.

This is interesting since DTC brands have only recently entered the mainstream in the UK. But clearly, UK shoppers have been positive about DTC offerings for a while, given that 'Health & Beauty' (29%) is the second-most purchased category internationally. This presents a ripe DTC opportunity for non-UK supplement brands trying to enter the UK market, as many established brands have already realized.

FMCG giants like Nestle and Unilever have been entering the supplement space by acquiring leading DTC brands. To give you a few examples

- Nestle Health Science’s acquisition of Persona™, a subscription-based vitamin company offering personalized products.

- Bicodex Group acquired Hilma, a company specializing in natural digestive remedies.

- Unilever has acquired Onnit, a holistic wellness and lifestyle company renowned for its Alpha Brain supplement. This is one of the seven fast-growing lifestyle brands in Unilever's billion-dollar wellness portfolio.

These big-name acquisitions send a positive signal for the global supplement market and vouch for DTC as a distribution channel with a rising potential. As Jostein Solheim, CEO of Unilever’s Health & Wellbeing business, concurs in his remarks about their wellness portfolio:

“Our business contribution from eCommerce is 1.6x the category average, and it’s getting bigger.

More than 50% of growth in this [supplements] category is projected to come from eCommerce, and we’re in a great place with our brands. They’re established in digital and direct-to-consumer channels and very connected to their users, so they can understand what they want and need.”

It's not just legacy brands that have caught the whiff of DTC success. Many digital-first DTC brands are also following suit. Bloom Nutrition, a US-based health supplement brand, has become a textbook example of successful UK expansion.

How Bloom Nutrition broke into the UK market

When expanding operations on British land, Bloom Nutrition was mired with challenges, such as import and sales taxation, local label regulations and compliances, logistics operations, inventory management, and more.

Bloom made three strategic moves to reach and thrive on UK soil:

1. Led by Bloom Nutrition's founder, Mari Llewellyn, they have built a “community brand” through social media marketing.

They've attracted and captured the attention of a global audience, including the Brits, primarily through TikTok and other social channels. To bank on this surging global demand, they:

- Improved their D2C website experience for British audiences with localized pricing, email notification engines, FAQs, etc.

- Strengthened their local presence by investing in PPC-driven targeting, listing optimization, and inventory replenishment

2. Nutrabolt’s acquisition of a 20% minority stake in Bloom Nutrition for $90 million provided the financial backing they needed to expand. It also gave them the resources to collaborate with operation partners and swiftly navigate the compliance and taxation landscape.

And the bonus PR following the acquisition was another notch in its belt: “They’ve built a strong brand and business over the past 4.5 years, yet there is whitespace to pursue in the form of new product platforms and distribution opportunities.”—Doss Cunningham, chairperson and CEO of Nutrabolt

3. Expansion from DTC channels into omnichannel retail via Walmart, Target, and Amazon helped Bloom diversify its distribution channels and improve sales.

They've been in the trade for a year, and they’re doing remarkably well. Bloom Nutrition had nine figures in sales in 2023, exemplifying the promising potential of DTC in the UK.

Conclusion: A market ripe for growth

The numbers paint a clear picture — the UK's supplement market is booming, and how!

We notice four major submarkets on the rise: plant-based probiotics, sports nutrition, green products, and personalized supplements, which are attracting brand investments and fanfare on social media from consumers.

Regulatory frameworks around product labeling, consumer safety, and fast delivery remain major business concerns. However, brands are setting up fulfillment centers and outsourcing fulfillment operations to tackle the challenges of expansion and distribution faster.

Despite the challenges, one thing is clear: The UK’s dietary supplement market is ready and ripe for growth.The United Kingdom’s dietary supplement market, valued at $718 million, might seem like a gentle giant compared to the US’s $4.58 billion and China’s $5.33 billion behemoths. However, despite the seemingly modest number, there's more to the UK's supplement market than meets the eye.